By Patrick Ma, Director of Listed Products, Admiral Investments

Feb 6, 2024 – Following a rally in the fourth quarter of 2023, the capital markets had a subdued start to 2024. US economic data indicated a potential soft landing, with fourth quarter 2023 real GDP growth hitting 3.3% compared to the consensus estimate of 2%, and employment figures surpassing market expectations.

Responding to this, Federal Reserve officials adopted a more hawkish stance to temper market anticipations of aggressive rate cuts. Although the Fed maintained the Fed fund rate at its current level during the January FOMC meeting, Fed chairman Powell indicated that a rate cut in March was unlikely. Throughout January, the US 10-year Treasury bond yield rebounded from its end-2023 low of 3.87% to hover around the 4% mark. Notably, the USD index surged from 101.3 at the end of 2023 to 103.2 by January 2024.

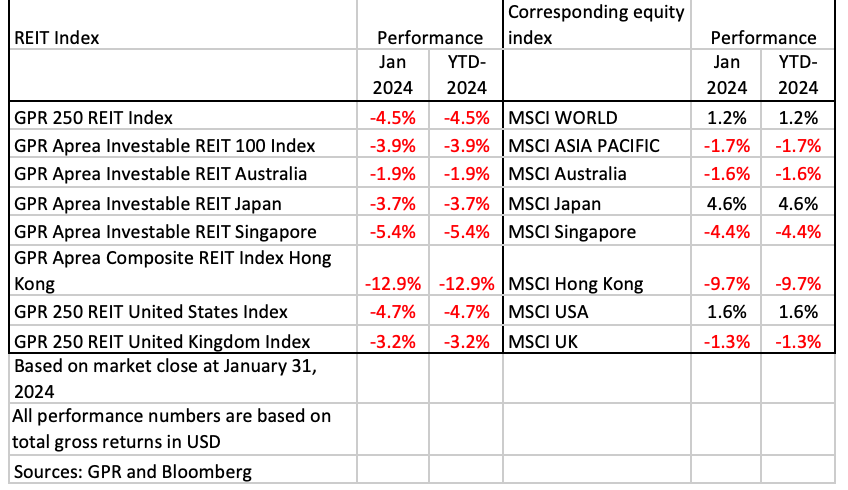

The dampening of rate cut expectations hampered the global stock market rally, particularly affecting Asia Pacific markets. While global equities saw a modest rise of 1.2% in January, equities in the Asia Pacific region dropped by 1.7%. The global equity rally was predominantly fuelled by gains in the US and Japanese stock markets. The sustained rally in tech-related stocks, notably the “Magnificent 7,” contributed significantly to the strength of the US stock market. Meanwhile, investor interest in the Japanese equity market was bolstered by expectations of the country ending its zero interest rate policy and exiting the deflationary era.

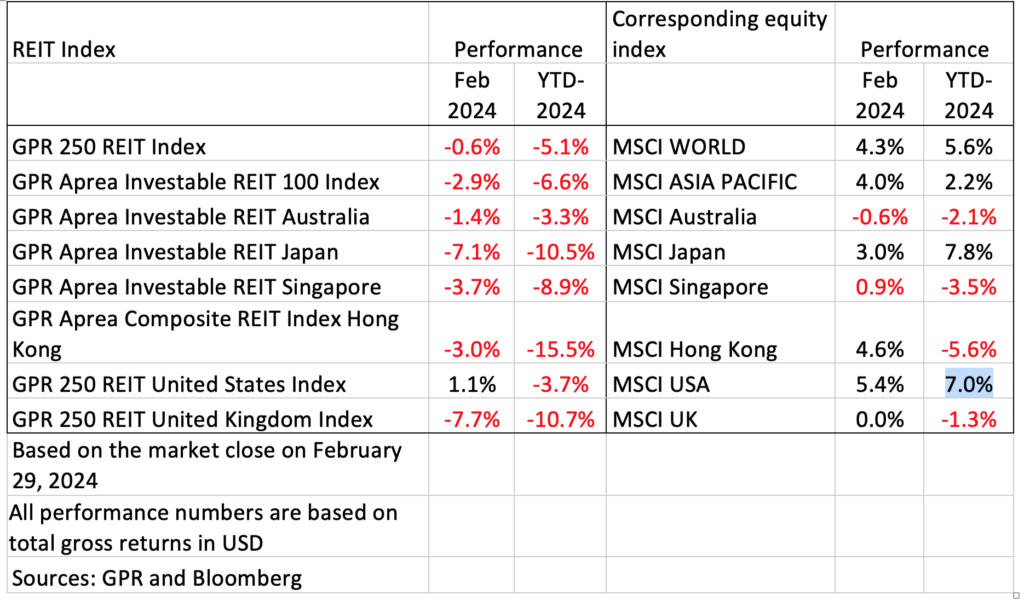

The diminished prospects of a Fed fund rate cut weighed on the performance of global REITs, which declined by 4.5%. Asia Pacific REITs dropped 3.9%. Despite relatively strong performance in local currency terms, Australian and Japanese REITs suffered from currency translation losses due to the strengthening USD. Australian REITs benefited from a pause in the Reserve Bank of Australia’s cash rate hike, particularly boosting retail REITs and homebuilding-related plays like Mirvac and Stockland. Among Japanese REITs, hotel and office sector REITs benefited from a rebound in tourism and capital influx from overseas investors, respectively. Hong Kong REITs were the worst performers, influenced by uncertainty surrounding China’s economic outlook.

Looking ahead, the market is likely to continue adjusting to the prospect of less aggressive US interest rate reductions, resulting in firmer US interest rates and a stronger USD. This combination poses challenges for Asia Pacific REITs. However, except for the Bank of Japan, central banks in the Asia Pacific region are expected to commence their rate-cut cycles this year. Additionally, expectations of the Bank of Japan’s exit from its zero interest rate policy should bolster the outlook for Japan’s real assets and, consequently, REITs.