Star Asia’s Proposed Bid For Sakura Sogo Challenges Japan-REIT Regulations

Fund managers regard Star Asia Group’s bid for Sakura Sogo as a positive move. More importantly, they see it as a legal test of the J-REIT framework. August 30 will be a key date for Sakura Sogo unitholders and regulators.

Amid Japan’s typically amicable REIT culture, Star Asia Group’s takeover proposal for Sakura Sogo on May 10 was an unexpected move. For the first time, a provision in the J-REIT legislation that allows a unitholder with at least a 3% holding for a minimum of six months to table a proposal and call for an extraordinary meeting has been evoked. Star Asia Group, which has a 3.6% stake in Sakura Sogo REIT through its affiliate Lion Partners, has asked for a meeting to remove Sakura’s existing executive director, and for its asset manager to be replaced by Star Asia’s asset manager. Also, for the first time, a J-REIT regulation known as Minashi, by which non-votes are counted as “yes” votes, will be tested on August 30, when Sakura Sogo’s unitholders will vote on Star Asia Group’s bid.

“Whatever the outcome, J-REITs that are facing challenges in achieving growth on their own and have low market assessments of the value of their property holdings could also become the subjects of takeover proposals,” says UBS’s Tokyo-based analyst Kazufumi Takeuchi.

“This possibility could lead to further efforts to strengthen governance and raise their share prices through buybacks,” he says. Takeuchi also believes that the recent events could prompt similar proposals and serve as a positive stimulus for the sector.

To track the events of the takeover bid, please click on TIMELINE: Tracking the developments of Star Asia’s controversial bid for Sakura Sogo

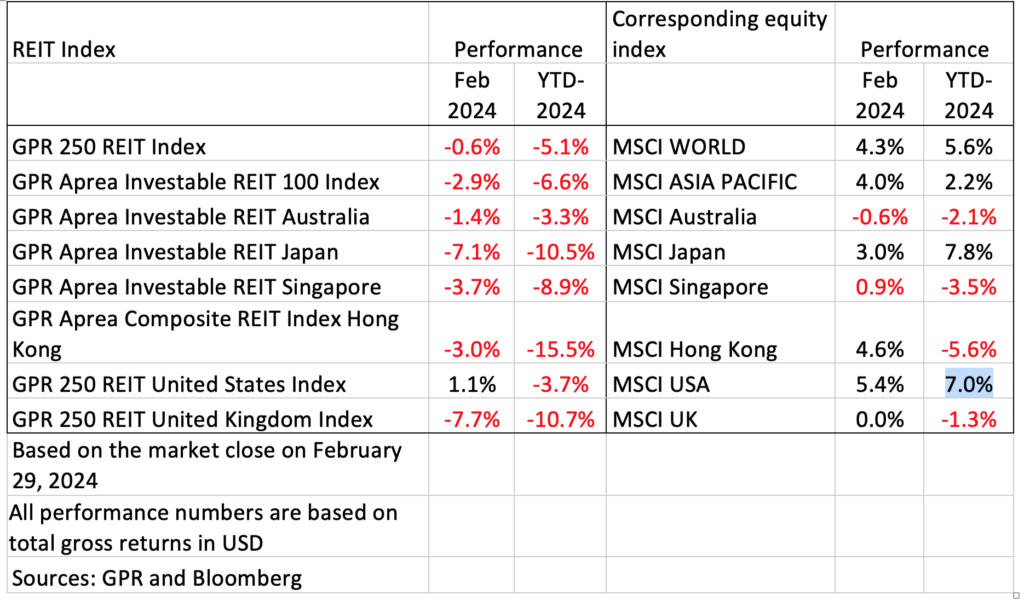

For J-REIT rules, click here. For J-REIT performance chart, click here.

Tim Gibson, Co-Head of Global Property Equities, Janus Henderson Investors, has similar views. “This is an important test of the legal framework, as well as Japan’s resolve to improve corporate governance,” he says, adding that these rules have been in place for some years.

“If shareholders review the deal and conclude this is not in their best interests, then they are of course free to vote against,” he says.

Mirai will potentially absorb Sakura

Sakura Sogo, which manages about 56 billion yen (US$518 million) worth of assets, has spurned Star Asia Group’s offer and announced that it is in friendly merger talks with Mirai Corporation, whose sponsors are Mitsui & Co. and IDERA Capital Management. Mirai confirmed the discussions and said their counter-proposal will give unitholders a “clear and tangible option” to consider. Mirai said their merger scheme will also be an “absorption-type,” with Mirai being the surviving entity and Sakura Sogo being the absorbed entity after the deal.

Fund managers are generally supportive of a combined Star Asia-Sakura Sogo entity. “Star Asia’s proposal makes sense for both shareholders of Star Asia and Sakura. Companies that can add value by growing earnings and dividends will continue to enjoy a lower cost of capital advantage,” says Gibson.

“Over the years, Star Asia have proven their ability to execute, not just buying but also selling. Unfortunately for Sakura, their track record in these areas is somewhat mixed at best. This undermines their counter-arguments,” says Gibson.

Some fund managers favour Star Asia over Mirai

Daniel Feldmann, a senior analyst at Timbercreek Asset Management, also favoured Star Asia Group’s merger proposal over Mirai’s. In his three years of coverage for Mirai, Feldmann said the company has been found to have debatable asset allocation decisions and weak shareholder alignment. Mirai, a Chinese-Japanese joint venture, also has the disadvantage of trading at a significant discount as certain investor groups do not fully understand or trust the Chinese backed J-REIT structure, he says.

“Just from a simple business combination point of view, I do not believe that there is going to be additional shareholder value created through a Mirai-Sakura Sogo REIT. I am very positive that Star Asia, as a significant shareholder of Sakura Sogo, can create more shareholder value in the long run in taking over the management of the combined vehicle,” says Feldmann.

In terms of Star Asia managing two REITs with similar mandates, Feldmann says that this is not something new, and that there are other groups that are managing different REITs as well.

Investors will be watching the events on August 30. In the morning, Star Asia Group will host its Sakura Sogo’s unitholder meeting. In the afternoon, Sakura Sogo will convene a separate meeting with its unitholders to decide on its proposed merger with Mirai.

Due to Minashi, a vote count could be in Star Asia’s favour if some retail investors choose not to turn up to vote. As at December 2018, Sakura Sogo has a 53.5% retail unitholder base.